Equity Market Outlook

|

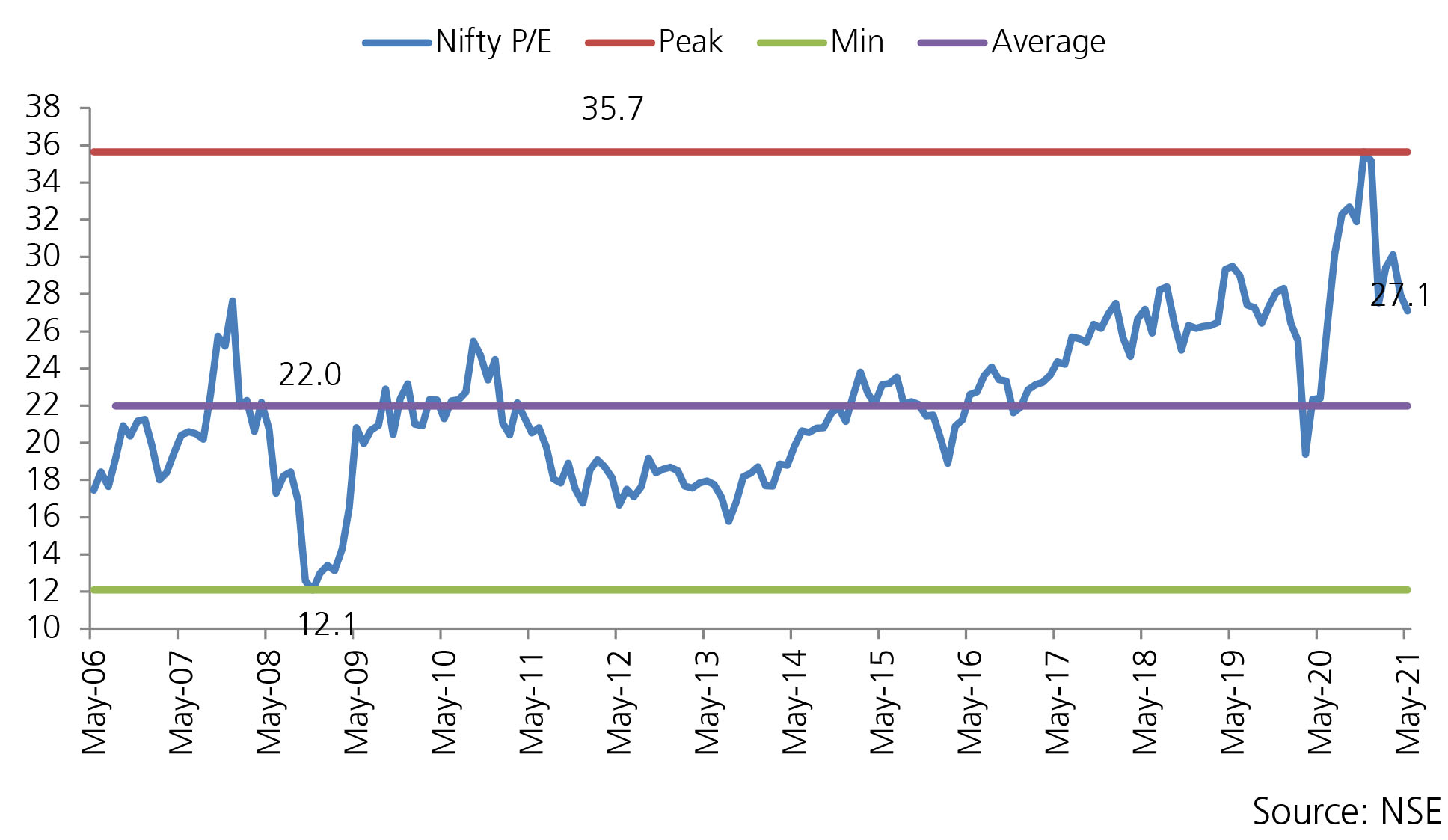

AS ON 31st May 2021

|

● Growth: 4Q GDP (+1.6%) came ahead of expectations (details here). But second wave led restrictionsdragged activity indicators back to Jun’20 levels (details here), prompting IMF to revisit its +12.5% forecast for FY22E.

● Lockdowns: Even as the Covid situation seemed to be coming under control, some states like Maharashtra, Tamil Nadu, Kerala and Goa took a cautious stance and extended the strict restrictions by a fortnight.

● Vaccination: Around ~17% / ~5% of India’s adult population had received the first / both doses of Covid vaccines by the last week of May. Daily momentum, however, had fallen to ~2mn/day in May vs ~3mn/day in April. However, in June it is expected that the country will vaccinate more than 10 Cr people since supplies from the vendors is expcted to increase.

● Earnings: IMost Nifty companies (c.90%) have reported Q4 earnings. Within Financials, SBI delivered an asset quality beat. 4Q operating profit at +25% y/y was aided by recoveries in Bhushan Steel, partly offset by interest reversals. KMBs 4Q21 net income missed expectations on higher provisions on the investment book. In the consumers’ space, both Tata Consumer’s and GCPL’s Q4 earnings missed estimates on lower margins even as revenues were in line. Dabur’s Q4F21 operating performance was underwhelming with revenue and EBITDA missing forecasts. Within autos, while high commodity prices impacted margins, price hikes, cost reduction efforts and improved mix aided in better results. Among the large names reporting in May, Hero and M&M (tractor) beat consensus earnings expectations, while Eicher and Tata Motors’ earnings were broadly in line. In metals, Tata Steel reported a 49% YoY increase in sales helped by strong demand and price hikes. Cement companies declared better results despite rise in raw material cost driven by healthy revenue growth. Separately, APNT reported a significant revenue beat in Q4, even as higher COGS/other expenses weighed on EBITDA.