Equity Market Outlook

|

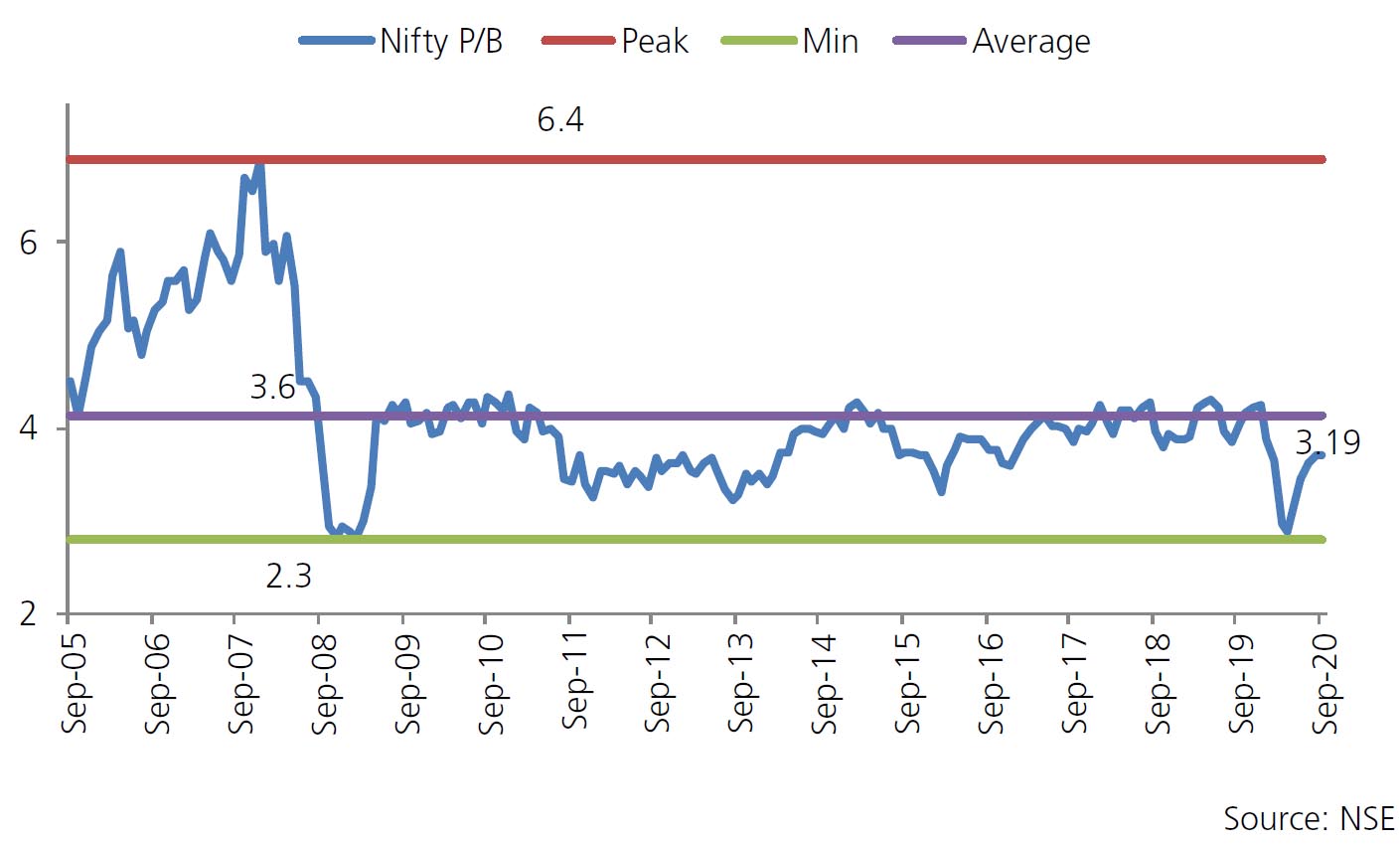

AS ON 30th September 2020

|

Deal momentum steady in Sept with 18 deals of ~USD1.6bn (vs 19 deals worth ~USD8.1bn in August) incl. a slew of IPOs - CAMS (~USD305mn), Happiest Minds (~USD95mn), Route Mobile (~USD80mn) and Blackrock’s stake sale in Essel Propack (~USD250mn).

● Farm Reforms: Rajya Sabha (Upper House) passed three farm bills aimed at reducing the control of middle men on the farmers and to improve farm incomes.These bills will give farmers more liberty with regards to whom and where they can sell their produce, enter into contract for selling their produce thereby removing uncertainty from their realisation and removing many items from essential commodities act therby encouraging creation of storage facilities for the farm produce. Governement has also announced MSP hikes in 6 rabi crops a month ahead of schedule.

● Labor Laws: Lok Sabha (Lower House) passed three labor bills that allowed businesses flexibility in hiring, retrenchment, making industrial strikes difficult besides facilitating ease of doing business and expanding social security net. These should help setting up of units by multinational companies as well as encourage smaller firms to achieve larger scale.

● Make in India: Government was reportedly planning incentives worth ~USD23bn to attract companies to set up manufacturing units in the country. After mobile phones / pharma, the PLI (production linked incentives) scheme could be extended to autos, solar panel and consumer appliances manufacturers to attract supply chains moving away from China.

● Unlock 5.0: Ministry of Home Affairs issued the new unlock guidelines wherein they allowed cinema / multiplexes to open with 50% capacity, removed limits on outdoor gatherings and mulled re-opening of schools from October 15.

● Monsoon: Cumulative rainfall is tracking +9% ahead of the long-period average (LPA) levels on an aggregate basis (over June 1 – September 30, 2020). Out of the 36 meteorological subdivisions, rainfall has so far been excess / normal in 31 meteorological subdivisions and deficient in 5. North West India (-16% vs LPA) is lagging while Southern Peninsula (+29% vs LPA) and Central India (+15% vs LPA) and Eastern India (+6% vs LPA) have received higher than normal rainfall.

● Covid 19: Daily new COVID-19 cases have averaged ~87k in September vs. ~64k in August. However, the daily case count which increased to 90k+ cases for 11 consecutive days during the month, has now declined to ~83k cases (average of last seven days). Globally, India has the third highest number of deaths at ~99k behind US and Brazil. However, the mortality rate has been trending lower at ~1.6% (vs. 1.9% in August) while recovery rate continues to pick up ~83% (vs. ~75% at end-August). COVID-19 continues to broaden its geographical reach within the country. ICMR’s second sero survey stated that ~7.1% of the adult population is estimated to be exposed to COVID-19. A considerable population is still vulnerable and susceptible to COVID-19. Further, ICMR noted that the risk in urban slums is twice than that in non-slum areas and four times the risk in rural setting.