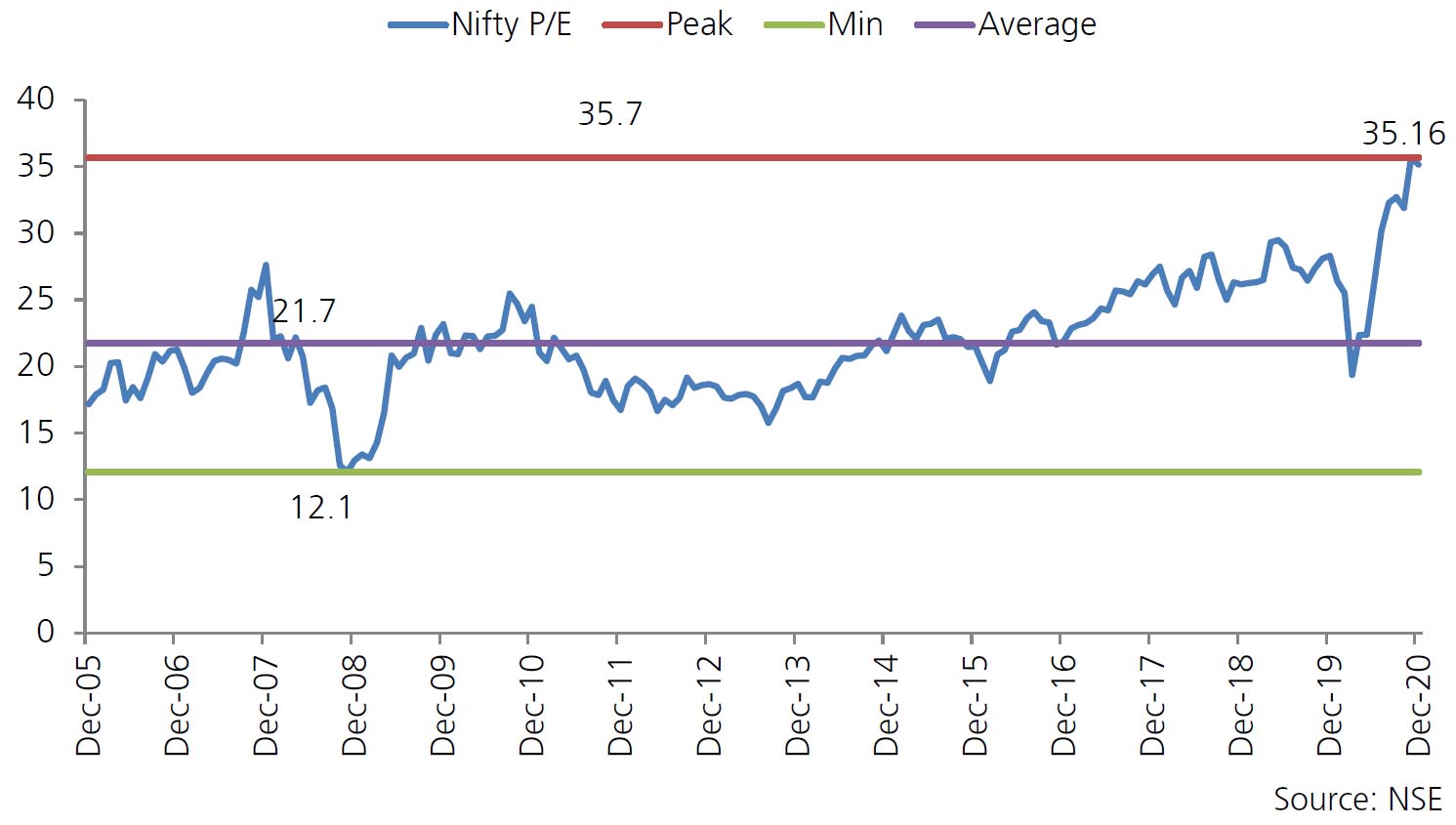

Equity Market Outlook

|

AS ON 31st January 2021

|

Deal activity picked up in December with 14 deals of ~USD2.7bn executed (vs 5 deals worth ~USD1.2bn in Nov) with key ones being IRCTC OFS (~USD598mn), QIPs of PNB (~USD512mn), Embassy REIT (~USD500mn), Canara Bank (~USD271mn), IDBI Bank (~USD195mn) and IPOs of Burger King (~USD110mn) and Mrs. Bectors Food Specialities (~USD73mn).

● Earnings: For 3QF21, the markets are expecting a pretty good set of numbers from Corporate India since the demand in the festive season has been very good for almost all the sectors. The shift in market share from unorganised to organised will likely continue in this quarter as well given that the supply chain of the unorganised is still broken and in some cases even if the supply chain is fixed, the distributors have stuck with the organised sector.

● Fiscal Stimulus: In a virtual pre-budget consultation meeting, representatives of India Corporates suggested lowering direct tax rates, incentives for housing sector, rationalization of GST & accelerating infra investments / privatization.

● Privatization: Government expressed confidence of completing divestments of BPCL and Air India after former received EOIs from three players (Vedanta + 2 PEs) whereas latter from players including Tata Group and a US based fund.

● Domestic Manufacturing Push: Payment and Overtime related issues at a new factory of Wistron, a Taiwan based contract manufacturer, resulted into labor unrest and suspension of production at the company’s plant in South India.

● Farm Reforms: Protests in the North against the contentious farm laws intensified in December as farmers blocked multiple routes into Delhi even as multiple rounds of talks with the government failed to fully resolve the deadlock.

● GST: GST collections for November (collected in December) were at an all-time high aided by improving economic activity, festive demand impact, and better compliance. GST collections were supported by normalization of economic activity accompanied by festive demand along with improved compliance associated with recent system changes and drive against GST evaders and fake bills. Based on the PIB release, total GST collection was at Rs1,152 bn for November (11.6% yoy) compared to Rs1,050 bn in October. Gross GST collections up to 9MFY21 were at Rs7.8 tn—contraction of 14.1% over 9MFY20.