Equity Market Outlook

|

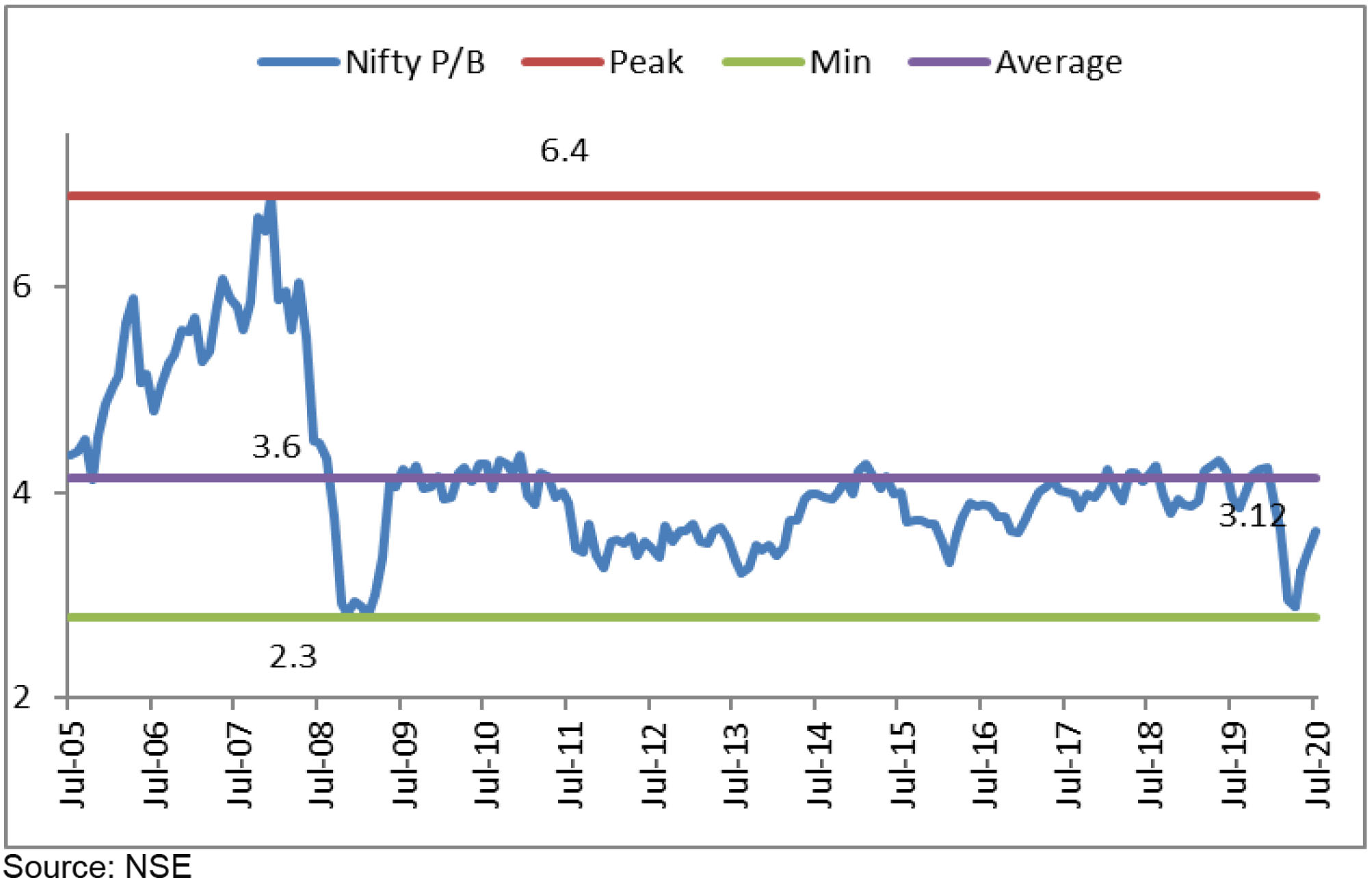

AS ON 31st July 2020

|

Deal momentum moderated slightly in July with 9 deals worth ~USD2.9bn (vs 11 deals of ~USD3.8bn in June), notable ones being Yes Bank’s FPO (~USD2bn), PI Industries’ QIP (~USD267mn) and Rossari Biotech’s IPO (~USD67mn).

● Monsoon: A good start in June was followed by an erratic July – rainfall across India was 9% below normal with a deficit of 20-27% in parts of northern, central and western India. Given that farmers had sped up crop planting in June in anticipation of a good season, if rainfall does not recover in the next few days it could raise concerns about the crop output

● Politics-Rajasthan Assembly: After Mr. Scindia’s exit early in the year, Congress faced another setback when the Former Deputy CM of Rajasthan Sachin Pilot and around 18 lawmakers in his camp rebelled against the Ashok Gehlot government. Congress moved to disqualify the members but the state High Court stayed the disqualification proceedings

● Lockdown: The Union Home Ministry announced guidelines for Unlock 3.0 wherein night curfew removal and re-opening of Yoga Institutes, Gyms is planned. Metro Rail, Theatres, Bars, Auditoriums, Entertainment parks will still remain prohibited. However, state imposed restrictions continued in certain states like Maharashtra, with Bihar being latest among the states extending lockdowns

● Earnings : So far 31 companies out of 50 in the Nifty Index have reported 1QFY21 results. 42% of the companies beat consensus estimates with a similar number missing estimates and balance inline. On aggregate basis revenue/EBITDA/PAT growth for 1QFY21 is at -28%/-1%/-40% Y/Y respectively. The sizeable aggregate PAT de-growth is due to Bharti Airtel reporting loss of Rs.152bn as the company provided for AGR dues. Excluding the aforementioned disproportionate loss, the aggregate PAT decline was -18% Y/Y.