Savings Plan

A savings plan is a reliable financial instrument that helps individuals build wealth gradually while maintaining a sense of financial stability and security. By committing to regular contributions, a savings plan enables long-term financial growth along with life insurance protection. ... It is an ideal choice for those seeking a disciplined approach to savings, offering assured returns and tax benefits. Be it planning for your future, your child's education, or retirement, saving plans serve as a smart tool to achieve your life goals with confidence. Read more

Kotak Assured Savings PlanBestseller

Pay ₹10,000/month for 10 years

Get

₹26,40,213 Lakhsafter 20th year

Death benefit/Life cover upto:

₹26,40,213 Lakhs#

Guaranteed@Returns

Kotak Guaranteed Fortune Builder

Pay ₹1,00,000 year for 10 years

Get(at the end of 11thyear)

₹1,15,236/year for 25 years

Life cover/death benefit:

₹13,20,000$

Plan Option: Income Only

Amit Rajeis an experienced marketer who has worked in various Fintechs and leading Financial companies in India. With focused experience in Digital, Amit has pioneered multiple digital commerce in India. Now, close to two decades later, he is the vice president and head of the D2C business department. He masters the skill of strategic management, also being certified in it from IIMA. He has challenged his challenges and contributed his efforts in this journey of digital transformation.

Prasad Pimplehas a decade-long experience in the Life insurance sector and as EVP, Kotak Life heads Digital Business. He is responsible for developing user-friendly product journeys, creating consumer awareness and helping consumers in identifying need for life insurance solutions. He has 20+ years of experience in creating and building business verticals across Insurance, Telecom and Banking sectors

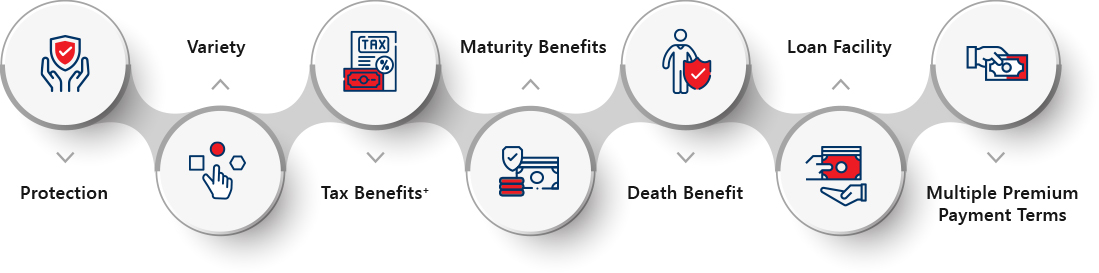

What are Savings Plan?

Savings plans are financial solutions that help you set aside money regularly to prepare for future needs while offering life insurance protection. These plans foster disciplined saving habits and offer a combination of security and returns. A savings plan can help you accumulate a huge corpus over time, ensuring you're financially prepared for life goals such as buying a home, funding your child’s education, or planning for retirement.

Most savings plans come with a maturity benefit that is paid out at the end of the policy term. Some also offer regular income options, giving you greater control and flexibility. In addition to financial growth, saving plans provide insurance coverage, offering peace of mind for you and your family in case of unforeseen circumstances.

Many plans can be customized with add-ons like critical illness coverage or accidental death benefits, making them a well-rounded financial solution. Whether you’re looking for stability, growth, or protection, choosing the best savings plan aligned with your financial goals can help you move forward with confidence.

Invest in a Savings PlanWhy Invest in a Savings Plan?

Investing in a savings plan is a practical step toward achieving long-term financial security and stability. These plans not only help you build a disciplined savings habit but also ensure that you are better prepared for unexpected life events. Be it dealing with medical emergencies, buying a house, or supporting your child’s education, a well-chosen savings plan empowers you to meet these goals without financial strain.

Savings plans are especially valuable for retirement planning, as they help you create a financial cushion for your golden years. By starting early and selecting a plan that suits your financial goals and risk profile, you can gradually build a strong foundation for a worry-free future. A proactive approach of saving today can lead to a secure and fulfilling tomorrow, for you and your loved ones.

Best Savings Plans in India

Choosing the right savings plan is essential for managing your money well. This can help you prepare for emergencies and plan for your future needs. In India, you have many options, from traditional ones like fixed deposits to more modern choices like mutual funds. Here's a simple look at these options:

Fixed Deposits

Fixed Deposits (FDs) are a traditional savings option that offer stable returns at fixed interest rates over a chosen term. They ensure capital protection and are insured by DICGC (Deposit Insurance and Credit Guarantee Corporation) up to ₹5 lakhs, making them one of the safest investment choices.

FDs typically earn higher interest than regular savings accounts and are ideal for conservative or short-term investors. You can invest for durations ranging from 7 days to 10 years, and while premature withdrawals are allowed, a small penalty may apply depending on the financial institution's terms.

Recurring Deposits

Recurring Deposits (RDs) let you invest a fixed amount every month for a specific period, earning interest on your savings. They’re ideal for those who prefer disciplined, gradual saving. RDs offer flexibility in choosing the tenure and deposit amount, making them accessible for different income levels.

Interest rates are fixed and generally higher than savings accounts. This investment suits individuals aiming to build a secure financial cushion over time without risking their capital. Early withdrawals are possible but may attract a nominal penalty depending on the bank’s policy.

Public Provident Fund (PPF)

Public Provident Fund (PPF) is a government-backed savings scheme ideal for long-term financial planning. With a 15-year lock-in, it offers guaranteed, risk-free returns and allows partial withdrawals or loans against the balance.

Contributions up to ₹1.5 lakh annually qualify for tax deductions under Section 80C, and interest earned and maturity proceeds are also tax-free. You can invest as little as ₹500 a year, making it accessible to all income levels. PPF is well-suited for those seeking safe, tax-efficient retirement savings with steady growth.

National Savings Certificate (NSC)

National Savings Certificate (NSC) is a fixed-income investment backed by the Government of India, available at post offices nationwide. With a five-year lock-in period, NSCs offer guaranteed returns and full capital protection, making them a safe option for risk-averse investors.

The interest is compounded annually and reinvested, boosting overall returns. These investments qualify for tax deductions under Section 80C, and there’s no upper limit on how much you can invest. While it may not beat inflation, NSC ensures steady growth and stable income for medium-term savings goals.

Sukanya Samriddhi Yojana (SSY)

Sukanya Samriddhi Yojana (SSY) is a government-supported savings scheme aimed at securing the future of girl children under the 'Beti Bachao, Beti Padhao' initiative. It allows parents or guardians of girls aged 10 years or younger to invest for goals like education and marriage.

SSY currently offers a high interest rate of 8.2% per annum, compounded annually, with tax benefits under Section 80C. The scheme is also triple tax-exempt, offering deductions on contributions, and tax-free interest and maturity proceeds, making it ideal for long-term, tax-efficient saving.

Employee Provident Fund (EPF)

Employees’ Provident Fund (EPF) is a compulsory savings scheme designed to help salaried individuals build a retirement corpus. Both employer and employee contribute a fixed percentage of the salary each month.

EPF is managed by the Employees’ Provident Fund Organisation (EPFO) and offers tax benefits under Section 80C. It ensures long-term savings with risk-free returns and is transferable between jobs. The funds can be withdrawn at retirement or partially during emergencies like home purchase or medical needs, making it a flexible and secure retirement planning tool.

Mutual Funds

Mutual Funds pool money from several investors to invest in a diversified mix of assets such as stocks, bonds, and other securities. These funds are managed by professional fund managers who aim to maximize returns based on the fund’s objective.

Mutual funds cater to various risk appetites, ranging from conservative debt funds to aggressive equity funds. They offer liquidity, transparency, and potential for long-term capital growth. While returns are not guaranteed, the diversification helps reduce risk, making them suitable for investors looking to grow wealth steadily over time.

Unit-Linked Insurance Plans (ULIPs)

Unit-Linked Insurance Plans (ULIPs) are hybrid financial tools that offer both life insurance and investment opportunities in one plan. A portion of your premium provides life cover, while the remaining is invested in market-linked funds like equity, debt, or balanced options.

ULIP plans allow fund switching based on your risk tolerance and market outlook. Ideal for long-term goals, they offer tax benefits and flexibility in investment strategy. ULIPs are suited for those seeking protection for their loved ones alongside wealth creation through disciplined, market-driven investments.

Monthly Income Plans

Monthly Income Plans (MIPs) are mutual fund schemes designed to provide consistent income while preserving capital. They primarily invest in debt instruments with limited equity exposure to generate better returns than fixed deposits, yet with relatively lower risk. MIPs are ideal for conservative investors seeking regular income with moderate risk.

Monthly saving plans offer flexibility in payout options, investors can opt for dividends, systematic withdrawals, or reinvestment through the growth option. Managed by professionals, MIPs offer diversification, regular income potential, and customization based on financial goals and risk tolerance.

Money Back Plans

Money Back Plans are insurance policies that combine investment growth with life coverage. They offer periodic payouts, which are a fixed portion of the total sum assured, paid to the policyholder at specific intervals during the policy term. At maturity, the insured receives the remaining amount plus any bonuses earned.

Additionally, if the policyholder passes away before maturity, their beneficiaries receive a death benefit separate from the survival payouts. This plan ensures steady returns while providing financial protection to the family.

Endowment Plans

Endowment plans are versatile life insurance policies that combine financial protection with disciplined savings. They offer life cover to safeguard your family’s future, ensuring financial support if you pass away unexpectedly. Simultaneously, these plans help accumulate a lump sum over time, ideal for goals like buying a home or funding education.

The maturity benefit is guaranteed and unaffected by market volatility, providing stability. Additionally, endowment plans offer flexible premium payment options: monthly, quarterly, yearly, or as a lump sum, making it easy to tailor the plan to your budget and needs.

Post Office (PO) Savings Scheme

The Post Office Savings Scheme is one of India’s safest and most trusted savings options, backed by the Central Government’s sovereign guarantee. It offers a fixed interest rate of 4% per annum, providing steady and secure returns.

With a low minimum deposit of just ₹500, it’s accessible for all savers. Ideal for cautious investors, PO savings accounts are perfect for parking surplus funds temporarily or saving towards short-term goals like buying a gadget or planning a vacation, ensuring your money grows with minimal risk.

Senior Citizen Savings Scheme (SCSS)

The Senior Citizen Savings Scheme (SCSS) is a secure, government-backed retirement savings plan for Indian residents aged 60 and above. It allows senior citizens to invest between ₹1,000 and ₹30 lakh for a five-year term, earning a fixed interest rate of 8.2% per annum.

The scheme features a straightforward application process and can be opened at authorized banks or post offices nationwide. Accounts are transferable between branches, offering convenience. Additionally, the maturity period can be extended by three years at applicable interest rates, enhancing retirement income stability.

Atal Pension Yojana (APY)

Atal Pension Yojana (APY) is a government-supported social security initiative designed to provide a guaranteed monthly pension to senior citizens. Built on the National Pension Scheme (NPS) framework, it offers retirees a fixed pension ranging from ₹1,000 to ₹5,000 based on their contributions during their working years.

The Central Government assures the pension, ensuring stable post-retirement income. Previously open to Indian citizens aged 18 to 40 with savings accounts and non-taxpayers, contributions vary according to the subscriber’s age and targeted pension amount.

National Pension Scheme (NPS)

The National Pension Scheme (NPS) is a flexible, market-linked retirement savings plan available to all Indian citizens. It offers a low-cost way to build a retirement fund through regular contributions managed by professional fund managers across equities, debt, and government securities. Subscribers must contribute consistently during their working years.

At retirement, a portion of the corpus can be withdrawn as a lump sum, while the remainder is used to purchase an annuity, ensuring lifelong pension income. NPS also provides extra tax benefits of up to ₹50,000 on voluntary contributions.

| Savings Plan | Returns / Interest Rate | Lock-in Period | Minimum & Maximum Premium Amount | Tax Benefits |

|---|---|---|---|---|

| Fixed Deposits (FDs) | Fixed interest, higher than savings accounts | 7 days to 10 years | Varies by bank, no fixed minimum | Interest taxable, principal under Section 80C if applicable |

| Recurring Deposits (RDs) | Fixed interest rate, higher than savings accounts | 6 months to 10 years | Monthly installments as per plan | Interest taxable, principal under Section 80C if applicable |

| Public Provident Fund (PPF) | Guaranteed returns, currently ~7.1% p.a. | 15 years | ₹500 to ₹1.5 lakh per year | Triple tax exemption: contribution, interest, maturity |

| National Savings Certificate (NSC) | Fixed interest, compounded annually, revised quarterly | 5 years | No maximum limit | Principal & interest eligible for deduction under Section 80C |

| Sukanya Samriddhi Yojana (SSY) | High interest, currently ~8.2% p.a. | 21 years or till marriage of girl child | Min ₹250, max ₹1.5 lakh per year | Triple tax exemption on deposit, interest, and maturity |

| Employees’ Provident Fund (EPF) | Risk-free, interest rate set by EPFO (~8.25% p.a.) | Until retirement (~58 years) | As % of salary, no fixed limit | Contribution and interest tax-exempt, maturity tax-free |

| Mutual Funds | Market-linked, varies by fund type | No fixed lock-in; exit load may apply | Min ₹500 SIP or lump sum varies | Equity funds: 1-year gains tax-free; Debt: indexation benefits |

| Unit-Linked Insurance Plans (ULIPs) | Market-linked, varies by fund | Typically 5 years | Premium depends on plan | Premium & maturity proceeds eligible under Section 80C |

| Monthly Income Plans (MIPs) | Debt-oriented, steady income, market-linked | No fixed lock-in | Minimum varies | Dividend income taxed as per slab |

| Money Back Plans | Fixed returns + bonuses | Typically 15–20 years | Premium varies | Premium under Section 80C, maturity generally tax-free |

| Endowment Plans | Guaranteed maturity sum | 10–20 years | Flexible premium frequency | Premium under Section 80C, maturity tax-free |

| Post Office Savings Scheme | Fixed 4% p.a. interest | None | Min ₹500 to open | Interest taxable, no deposit tax benefit |

| Senior Citizen Savings Scheme (SCSS) | Fixed 8.2% p.a. interest | 5 years (extendable 3 years) | Min ₹1,000, max ₹30 lakh | Deduction under Section 80C on deposit |

| Atal Pension Yojana (APY) | Guaranteed pension ₹1,000–₹5,000 | Until death or withdrawal | Contribution varies by age/pension amount | Contribution eligible under Section 80C |

| National Pension Scheme (NPS) | Market-linked returns | Till retirement (~60 years) | Min ₹500 per contribution | Up to ₹2 lakh tax deduction under 80C + 80CCD(1B) |

Importance of Buying a Savings Plan

Saving money is a necessity for everyone, regardless of income or lifestyle. The importance of a savings plan cannot be overstated, as a well-structured savings plan provides a disciplined way to set aside funds, helping you work toward your financial goals while ensuring long-term security.

Financial Safety Net: A savings plan

acts as a cushion during financial emergencies, ensuring you're better prepared for unexpected events without disrupting your lifestyle.

Wealth Creation:

These plans allow your savings to grow over time through guaranteed returns or market-linked benefits, helping you build wealth systematically.

Disciplined Approach:

With regular premium payments, savings plans promote consistent saving habits and align your finances with future goals.

Flexibility & Protection:

Many plans come with optional add-ons and life cover, offering customization and ensuring financial protection for your loved ones.

Choosing the best savings plan ensures you build a strong financial foundation and are prepared for both opportunities and challenges in the future.

How to Choose the Right Savings Plan?

Saving money is important for financial planning, helping individuals achieve their short-term and long-term goals. The best savings plan in India is the one that matches your requirements. To make an ideal decision, it is essential to consider various factors, including the important things to remember when investing in a savings plan, and align them with your financial plans.

Define Your Goals:

Identify your short-term and long-term financial goals, such as a child’s education, home purchase, or retirement, and choose a plan that aligns with these objectives.

Evaluate Plan Benefits:

Review the features, benefits, and payout options of different savings plans to find one that best suits your lifestyle and risk appetite.

Use Financial Tools:

Leverage tools like premium calculators to estimate your ideal coverage amount and premium based on income, expenses, and future needs.

Check Liquidity Options:

Opt for plans that offer partial withdrawal or loan features to ensure access to funds during emergencies without policy disruption.

Consider Add-Ons:

Look for plans that provide additional riders like critical illness or accidental cover to enhance overall protection.