Terms and Conditions for ULIPs

You may avail of tax benefits under Section 80C and Section 10(10D) of Income Tax Act, 1961 subject to conditions as specified in those sections. Tax benefits are subject to change as per tax laws. Customer is

advised to take an independent view from tax consultant.

The calculation is generated on the basis of information provided and does not constitute an offer or solicitation for the purpose of purchase or sale of any product. Further customer is the advised to go through

the sales brochure before conducting any sale.

Grace Period

- There is a Grace Period of 30 days for the annual, half-yearly and quarterly mode, and 15 days for the monthly mode from the due date for payment of premium.

- The policy stays in force during the Grace Period.

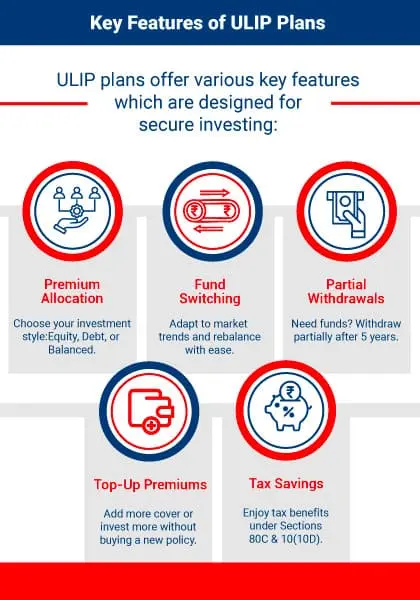

Partial Withdrawals

Some ULIP instruments offer you an option of partial withdrawals. There are various conditions under which this can be done, but it varies from product to product.

Rider Details

Applicable Rider Charges will be deducted from the Fund value if the Riders are chosen. There are different rider options that can enhance your protection and it is recommended that you check them out.

Free Look Period

If the policyholder does not agree to the terms and conditions mentioned in the policy document, he/she can always return the policy. This can only be done within 30 days of accepting the policy depending on

the channel through which the policy was bought. This period is called free-look period and the insurance company should refund the premium to the policyholder.

There are a few charges which can be deducted before the refund-

Goods and Services Tax and Cess

The premium figures are net of Goods and Services Tax and Cess, as applicable. Goods and Services Tax and Cess rates are subject to change from time to time as per the prevailing tax laws and/or any other laws.

Tax Benefit

Tax benefits are subject to conditions specified under the Income-tax Act, 1961. Tax laws are subject to amendments from time to time. Customer is advised to take an independent view from tax consultant.

Risk Factors:

The Unit Linked Insurance Products do not offer any liquidity during the first five years of the contract. The policyholder will not be able to surrender /withdraw the monies invested in Unit Linked Insurance

Products completely or partially till the end of the fifth year from inception.

Unit Linked Life Insurance products are different from the traditional insurance products and are subject to the risk factors. Please know the associated risks and the applicable charges (along with the

possibility of increase in charges), from your Insurance agent / Corporate Agent / Insurance Broker / Intermediary or policy document of the insurer. The premium paid in Unit Linked Life Insurance policies are

subject to investment risks associated with capital markets and the NAVs of the units may go up or down based on the performance of fund and factors influencing the capital market and the insured is responsible

for his/her decisions. All benefits payable under the Policy are subject to the Tax Laws and other financial enactments, as they exist from time to time.

This website content is not a brochure and only gives the salient features of the plan.

Kotak e-InvestUIN – 107L121V02, Kotak e-Invest; UIN – 107L121V02. This is a non-participating unit-linked life insurance individual savings product. Unit Linked Life Insurance products are different from

the traditional insurance products and are subject to the risk factors. For more details on risk factors, terms and conditions please read the sales brochure carefully before concluding a sale.

Kotak T.U.L.I.PUIN: 107L131V02. This is a non-participating unit linked Life Insurance Individual Savings Product.

Kotak Invest MaximaUIN: 107L073V05. This is a non-participating unit linked Life Insurance Individual Savings Product.

Kotak Single Invest AdvantageUIN: 107L065V05, This is a Non-Participating Unit-Linked Life Insurance Individual Savings Product.

Kotak PlatinumUIN No.: 107L067V07. This is A Non-Participating Unit-Linked Life Insurance Individual Savings Product.

Kotak Wealth Optima PlanUIN: 107L118V03 This is a non-participating unit-linked life insurance individual savings product. For more details on risk factors, terms and conditions, please read sales brochure

carefully before concluding a sale.

The assumed non-guaranteed rates of return chosen in the illustration are 4% p.a. and 8% p.a. These assumed rates of return are not guaranteed and they are not the upper or lower limits of what you might get back

as the value of your policy is dependent on a number of factors including future investment performance. The actual experience may be different from the illustrated. Please note that Bonuses are NOT guaranteed

and may be as declared by the Company from time to time.

Kotak e-Invest Plus;UIN - 107L137V02. This is a non-participating unit-linked life insurance individual savings product.

Kotak Confident Retirement Savings Plan – UIN: 107N162V01 This is a participating non-linked pension individual savings plan. For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale. This product is available for sale through online mode. Benefits under this plan are dependent upon the performance of the participating Funds. Please note that Bonuses are NOT guaranteed and may be as declared by the Company from time to time. The risk factors of the bonuses projected under the product are not guaranteed. Past performance doesn’t construe any indication of future bonuses. These products are subject to the overall performance of the insurer in terms of investments, management of expenses, mortality, and lapses.

Kotak Confident Retirement Builder – UIN: 107L136V02 This is a non-participating unit-linked pension individual savings product. For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale. This product is available for sale through online mode.

Section 41-

Extract of Section 41 of the Insurance Act, 1938 as amended from time to time states: (1) No person shall allow or offer to allow, either directly or indirectly, as an inducement to any person to take or renew or

continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy, nor shall

any person taking out or renewing or continuing a policy accept any rebate, except such rebate as may be allowed in accordance with the published prospectuses or tables of the insurer. (2) Any person making

default in complying with the provisions of this section shall be liable for a penalty which may extend to ten lakhs rupees.

Section 45-

Fraud Misstatement would be dealt with in accordance with provisions of Section 45 of the Insurance Act, 1938 as amended from time to time. Please visit our website for more details:

Read more about section38_39_45_of_insurance_act_1938

BEWARE OF SPURIOUS PHONE CALLS AND FICTITIOUS/ FRAUDULENT OFFERS

IRDAI is not involved in activities like selling insurance policies, announcing bonus or investment of premiums. Public receiving such phone calls are requested to lodge a police complaint.

Regd. Office: Kotak Mahindra Life Insurance Company Ltd. Reg No. 107; CIN : U66030MH2000PLC128503; Regd. Office: 8th Floor, Plot # C- 12, G- Block, BKC, Bandra (E), Mumbai – 400051 | Website: www.kotaklife.com |

WhatsApp: 9321003007 | Toll Free: 1800 209 8800 | ARN No. KLI/25-26/E-WEB/468

Trade Logo displayed above belongs to Kotak Mahindra Bank Limited and is used by Kotak Mahindra Life Insurance Company Ltd. under license.